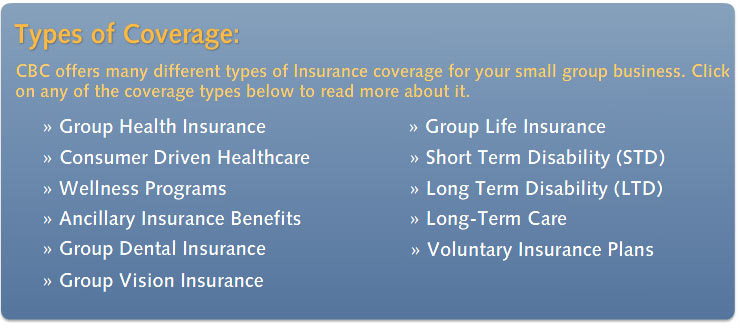

Group Health Insurance

Group health insurance comes in many forms. Plan selection will vary based on:

- Group Size (number of employees)

- Budget

- Employee needs

- Medical Conditions in the Employer Group

Traditional group health insurance comes in two types of plans:

- HMO - Health Maintenance Organization

- PPO - Preferred Provider Organization

HMO plans normally utilize a local network of physicians / hospitals and usually require the member to choose a primary care physician (PCP) for their standard healthcare. This doctor becomes your “gatekeeper” for all your medical needs. This is the doctor you call or see when you are sick, and he/she will refer you to a specialist or other provider within the HMO network if necessary. With most HMOs you will not receive benefits if you go out-of-network, except for emergency care.

- Staff Model HMO - A form of HMO in which doctors are employees of the HMO and you see them at a central medical facility.

- Individual Practice Associations (IPAs) - Here, an HMO contracts with outside physician groups or individual doctors who have private practices. This means the HMO network will include doctors in various locations rather than only at a central facility.

PPO plans also use a network of physicians, this can be a local and/or nationwide networks. In this system, you may seek treatment from an approved network of providers, or may see other providers outside the network. Members are not required to choose a primary care physician (PCP) and can access any PPO specialist without obtaining a referral for specialists. Traditionally care under a PPO is subject to deductibles and coinsurance.

POS Plans

A hybrid of the HMO and PPO is known as a POS (Point of Service) plan. Like a standard HMO, your primary care doctors make referrals to other providers within the plan. If you want to go to a physician outside the network without consulting your primary care doctor, the POS plan will pay a predetermined amount of the bill and your share of the bill will be higher than it would if you stay in-network. These plans usually cost more in monthly premiums than straight HMOs, but they give you the flexibility to access any doctor that you want even if out of network, though the reimbursement will vary.

[TOP]

Consumer Driven Healthcare (CDHC)

CDHC Plans are traditionally delivered through a PPO network. The difference is that members utilize personal or group Health Savings Accounts (HSAs), Health Reimbursement Arrangements (HRAs), or similar medical payment products to pay routine health care expenses directly to the providers, while a High Deductible Health Plan (HDHP) protects them from catastrophic expenses. Higher deductible insurance policies normally cost less, however the user pays routine medical claims using a pre-funded spending account. Access to this account is often provided through a debit card or checks that can be written on the account, and may be provided by a bank or insurance plan. If the balance in the account is exhausted, the user then pays claims just like under a regular deductible. Members keep any unused balance or "rollover" at the end of the year to increase future balances.

HSA Plans

Health Savings Accounts (HSAs) are a relatively new way for Americans to pay for their healthcare. Like an IRA, the money deposited into an HSA is completely tax-deductable. These accounts, however, can be accessed whenever individuals need them to pay for qualified healthcare expenses. In the meantime, their money earns tax-free interest for future medical costs.

For more information on HSA’s click here.

[TOP]

Wellness Programs

Wellness Programs are becoming an ever-growing area in the employee benefits arena. Research has found that a large portion of the rise in employee healthcare costs is due to preventable lifestyle choices by employees themselves. Wellness Programs can drive changes in employees’ behavior, positively affecting the corporate culture, benefit claims costs, and workers compensations claims costs.

[TOP]

Ancillary Insurance Benefits

Ancillary Benefits are a vital part of a comprehensive employee benefit program. Ancillary Benefits typically encompass: Dental, Vision, Life, Short Term Disability, and Long Term Disability Plans. Disability coverage is one of the most cost effective benefits a company can offer its workforce and provide important income protection for employers’ most valuable asset. Group disability plans can be offered through a choice of employer paid, employee paid or combination of employer/employee paid plans.

[TOP]

Group Dental Insurance

Group Dental Plans offer richer benefits and do not have the waiting periods typically found on individual dental plans.

[TOP]

Group Vision Insurance

Vision Plans differ from regular health insurance because they are a wellness benefit that helps defray costs of eye exams, eyewear, and other vision services and is not typically comprehensive. Many vision programs offer free exams and lenses while capping the amount that will be paid out on frames. Some Vision Plans utilize a doctor network while others use retail centers.

[TOP]

Group Life Insurance

Life Insurance plans are another inexpensive way to provide valuable insurance protection to a company’s employees. Group life insurance programs can vary greatly in the types and amount of coverage that is provided through the employer, or can be offered on strictly a voluntary basis.

[TOP]

Short Term Disability (STD)

Empowering employers to determine the benefit level that fits budgetary considerations as well as their employees’ needs, group STD insurance offers eligible employees income protection insurance coverage at competitive rates. Benefits under STD plans partially replace income lost as a result of an employee’s non-occupational accident or illness. In certain states, it is important to consider how benefits offered by the state will coordinate with employer sponsored plans.

[TOP]

Long Term Disability (LTD)

Long-term income protection insurance coverage at competitive group rates is but one advantage of LTD insurance. LTD pays monthly benefits to partially replace income lost as a result of a prolonged disability. Eligibility varies based upon an employee’s inability to perform the material duties of his/her occupation on a full-time basis or all such duties on a part-time basis as well as a loss in pre-disability earnings while working in any occupation. The length of payment schedules and size of payment benefits vary depending upon the duration of the disability and the employer’s size, respectively.

[TOP]

Long-Term Care

These cover medical care, nursing care and certain in-home care if you ever become unable to care for yourself due to an extended illness or disability. These plans can be offered employer paid, voluntary or the employer can choose to pay for a base amount and allow the employee to “buy up” to a richer plan.

[TOP]

Voluntary Insurance Plans

77% of employers offer Voluntary Benefit Programs that are fully paid by employees through payroll deduction.

As the U.S. health coverage environment evolves, working Americans are increasingly turning to voluntary employee benefits to supplement core coverage. Voluntary benefits can offer added financial security to employees, with no direct costs incurred by employers. Voluntary programs can include but are not limited to Limited Benefit Plans for Part-Time Employees, Critical Illness/Cancer Insurance, Disability Coverage, Universal and Term Life Insurance.

Since voluntary benefits are paid typically through payroll deductions and are chosen at will by the employee, there is no additional cost to employers. Voluntary Benefits can help:

- Attract and retain high quality employees

- Control the rising costs of group health insurance programs

- Educate the employees on the benefits package being provided to them

[TOP]